‘London Is Open’ is a three-part series from Cannabis Europa and Prohibition Partners, exploring the promising opportunities for successful medicinal cannabis and CBD companies listing on the London stock markets this year.

Supported by:

![]()

Part 2 – Legal & Compliance – Path to a Successful Listing

In this issue of the ‘London Is Open’ series, we will examine the regulatory process that medicinal cannabis and CBD companies need to be aware of, prior to a listing on London’s exchanges. This week the blog has been written in conjunction with the international commercial law firm Hill Dickinson LLP, who recently worked on the successful listing of Kanabo, providing in-depth regulatory insights of cannabis IPOs on London’s capital markets.

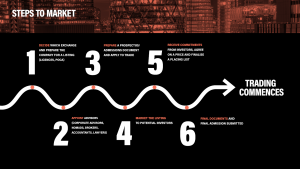

What are the key steps companies need to consider before listing?

The recent listings of Kanabo and MGC Pharmaceuticals on the LSE’s Main Market have attracted many cannabis-related businesses (CRBs), whether national or overseas, towards a potential listing opportunity on London’s capital markets. Although a listing is a fantastic opportunity for companies in the sector to harness investment and visibility, the decision to go public in London should be taken very seriously by CRBs as there are various caveats they need to consider.

According to Michael Bennett, a partner at the international commercial law firm Hill Dickinson, “it is important to prepare early on in the development of the business for an IPO if that is a preferred liquidity event for investors. This would include ensuring that the issuer is fully compliant with current Home Office guidelines and that it holds all relevant licences and consents in respect of its business activities”.

Along with holding all relevant licences (based on the nature of the applicant’s business and the jurisdictions where it operates), CRBs should appoint advisors suitable for the stock exchange they seek to list on. This includes corporate advisors, nominated advisors (NOMADs) in the case of a proposed AIM admission, brokers, reporting accountants and lawyers. Appointing the right set of advisors will help the company navigate the application and admission process, assist the company with the pricing of shares and independently review and report on the financial documents needed, and they will provide advice on any regulatory issues that can develop following the admission on the exchange.

Once a company has appointed its advisors, it is important to factor in the route to market and fundraising requirements so as to establish a well-thought-out timeline for a proposed listing. One of the key documents a company needs to prepare for a listing is a prospectus, or an admission document, which serves as a marketing and legal document that contains information on the company’s background and current business strategy, financials, initial offering, as well as any other relevant information an investor needs to make an informed investment decision. This also includes defining a set of “risk factors” in relation to the business, which are intended to provide prospective investors with an overview of the most salient risks related to that company, its prospects, the sector it operates within and any risks associated with its shares. Following the successful vetting of the prospectus or admission document by the appointed regulator or the responsible adviser (as the case may be), a company must successfully apply for the admission of its shares to trading.

Marketing the listing to potential investors is vital to gain as much attention as possible, and generate the investment needed for a successful IPO. Companies should choose their shareholder mix wisely and begin roadshows, promoting the investment potential through a series of investor meetings and pitches. Once commitments from investors (often varying in size depending on price) are received, a price should be agreed upon (based on demand and mix of investors within the price range) and a placing list should be finalised. Commitments by investors will be subject to the admission of the shares of the company to the relevant stock exchange and this is the final step before the company’s shares commence trading.

What is PoCA and why is it so important?

Since the legalisation of medical cannabis on 11 November 2018, there have been a number of companies seeking to list on various markets in London.

The regulators in London have adopted a cautious approach to the medical cannabis sector and prospective CRBs joining London markets. The Financial Conduct Authority (FCA) announced in September 2020, after an extensive review, its policies and guidelines in relation to the prospective listing of CRBs and the application of the Proceeds of Crime Act 2002 (PoCA). PoCA is designed to enable authorities to recover and confiscate the proceeds received from criminal activities and money laundering type offences, even where the conduct occurred entirely outside of the UK.

The relevance to the listing of a legal medical cannabis business may not seem immediately clear. In the UK, cannabis is a Schedule B controlled drug under the Misuse of Drugs Act 1971. UK companies may operate in the medicinal and pharmaceutical cannabis sector provided that they have the appropriate licences from the UK’s Home Office.

CRBs with operations occurring overseas looking to list may also be admitted if their operations abroad satisfy a PoCA risk assessment and the CRB is carrying on activities capable of being undertaken lawfully in the UK, pursuant to an overseas licensing regime that is similarly robust and effective.

Consequently, proceeds by companies that operate in the legal adult-use markets, found in Canada and the US, are viewed by the FCA as a PoCA risk because the cultivation, supply, production, and distribution of adult-use cannabis are criminal offences in the UK. It is therefore important for CRBs looking to list in London to be aware of the restrictions PoCA may have on their daily operations and determine whether their company is eligible for a listing on London’s capital markets (and whether the restrictions on the company post-listing are consistent with plans for the business’s future growth strategy.

The FCA’s announcement significantly narrows the number of large North American cannabis firms eligible to list on London’s primary capital markets, as many of these companies are active in the adult-use cannabis market. Overseas medicinal cannabis companies must therefore ensure that none of their activities or assets have any form of involvement in the adult-use cannabis market or risk being declared ineligible for listing.During our conversation regarding what issues overseas CRBs need to be aware of, Michael Bennett stated:

“The location of the issuer is a fundamental factor to consider prior to listing. If the prospective issuer is based overseas, that entity will be subject to a much higher degree of scrutiny and consequently the due diligence process will be more complicated as a result. If a prospective issuer is located in multiple locations, as we commonly find, it is critical to a well-run process that the issuer assembles a legal team with appropriate credentials in the sector. We have worked on several transactions with an international element and we are experienced in assembling and coordinating local advisors as part of an M&A or IPO-process.”

Which capital market? What are the initial listing differences?

Deciding on which stock exchange to list in London is very important, as each market has a set of key differences. Therefore, the decision to list on the LSE’s Main Market, AIM or the AQSE Growth Market will be determined by factors such as visibility, entry requirements, level of regulation, related players listed, and the size of the company.

LSE Standard Listing

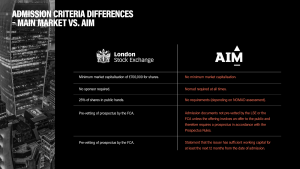

A company may approach a standard listing on the LSE’s Main Market if the goal is to enter the UK and gain as much visibility as possible. As the LSE’s Main Market is highly reputable, holding the FTSE 100 Index, the listing requirements on the LSE Main Market are the most onerous. The LSE’s Main Market is regulated by the FCA which vets and approves the prospectuses of companies that are seeking to list. For a standard listing for the Main Market, companies should draft a prospectus that includes their historical financial information covering at least three years, and it must be prepared in accordance with the UK Prospectus Regulation Rules. To obtain a listing, the prospectus must be vetted and approved by the FCA. The Company is also required to meet a number of standard eligibility requirements of the FCA and the London Stock Exchange. A company must also offer a minimum of 25% of shares to the public, otherwise, referred to as the “free float” rule. Shares that are held by directors and associates, or those with an interest of 5% or more, do not count as free-floating shares. A minimum market capitalisation of £700,000 is required for a company looking to list on the Main Market. The financial track record of the company must incorporate audited accounts of the last three years, be fully consolidated numbers and be no more than nine months old before the listing date. There are also admission fees to pay, which are dependent on market capitalisation of the company. The emergence of the cannabis companies entering the Main Market is very nascent; only three CRBs are listed on the LSE Main Market – Kanabo, MGC Pharmaceuticals and Zeotic.

AIM Listing

AIM is the growth-market segment of the LSE. Compared to the LSE, the market’s regulatory demands are simplified, which is suited to smaller growing companies. AIM is an exchange regulated market; thus, companies must abide by the rules of the exchange. Companies looking to list on this exchange need a NOMAD at all times. A NOMAD’s role is to advise whether a company is eligible for an AIM listing and guides a company through the listing process. The listing company must also make sure that they appoint and retain a broker, which could be the NOMAD or a securities house that is a member of the LSE. Companies must prepare an admission document, which is not typically vetted by the exchange. The applying company must have shares that are freely transferable and eligible for electronic settlement.

Compared to the LSE Main Market, AIM is viewed as more flexible and it allows a fast-track admission route for companies that already have been listed for 18 months on the top tier boards of the NASDAQ, NYSE and Australian Securities Exchange.

Although AIM might seem to be an intriguing market for CRBs to join, there has not been any official guidance for CRBs looking to list on the market. Jack Delaney, Senior Associate at Hill Dickinson notes that:

“AIM Regulation has yet to publish its own guidance for medical cannabis and wellness issuers, and as yet there has not been an IPO of a medical cannabis business on AIM. Our expectation is that AIM will adopt (formally or informally) its own criteria that is known and understood in the market in line with the FCA guidance and we hope that in 2021 AIM will welcome a first IPO of a medical cannabis issuer.”

AQSE Growth Market

The Aquis exchange is another market that is independent from the LSE and that promotes listings for small to medium-sized cap companies. Similar to the LSE, the AQSE has a Main Market and a Growth Market. The LSE and AQSE have similar admission requirements; however, there are some key differences. The AQSE Growth Market is of particular interest for CRBs as a handful of companies in the sector are already listed on the market such as Sativa Wellness Group, World High Life, Greencare Capital and Ananda Developments.

The Growth Market that competes with AIM is split into two segments, APX (Apex) and AXS (Access). The two segments have different levels of admission criteria, providing support for companies at different stages of their growth cycles. The Access segment is appropriate for companies undergoing early-stage growth whereas the Apex segment is intended for established companies with a stronger growth strategy.

Companies looking to list on the Apex segment are required to publish an FCA approved Growth Prospectus. The company must hold a minimum free float of 25% with at least 25 shareholders. It is also expected that an applicant’s securities have an aggregate market value of at least £10,000,000 in order to be admitted. Under an Apex listing, the company must provide a two-year consolidated trading history and have appointed two market makers, and issuers must comply with the QCA Code or the UK corporate governance code.

Compared to Apex, the Access segment has less onerous regulations, which is appropriate for smaller companies looking to go public. Companies looking to list on the Access segment need to provide an admission document and have a minimum market capitalisation of £700,000 for shares and £200,000 for debt or convertible securities. There is a minimum free-float requirement of 10%, and the issuer must have at least one market maker and one independent director.

The differences in the two AQSE Growth Market segments are varied enough for the CRBs in different stages of their growth cycle to make a fairly easy decision as to which segment would suit their growth best.

When asked about how the AQSE has dealt with previous CRBs listing on the exchange, Jack Delaney responded:

“The regulatory process for AQSE is similar to that of the FCA and AIM in a number of respects, and the requirement for detailed legal reports remains the same. Our clients have found the AQSE to be incredibly transparent and open in terms of their requirements. The regulator adopts a collaborative approach with issuers from an early stage in the process and this approach makes AQSE a welcoming destination in London for medical cannabis and wellness issuers.”

Making a final decision

A public listing is an important decision, and for CRBs it will take time and money to advance discussions and reach a point where they are confident they meet eligibility criteria, and can commit to a process confident there will be a positive end result. CRBs need to evaluate all their options regarding which market would suit them best. The best advice is early dialogue with advisers and regulators and to plan for a period of preparation ahead of any planned IPO.

In the next issue of London Is Open, in conjunction with Peterhouse Capital the series will examine the investment potential of a listing on London’s capital markets.

![]()

About Hill Dickinson

Hill Dickinson LLP is a leading and award-winning international commercial law firm with more than 850 people including 185 partners and legal directors. It has offices in Liverpool, Manchester, London, Leeds, Piraeus, Singapore, Monaco and Hong Kong.

The firm delivers advice and strategic guidance spanning the full legal spectrum, from non-contentious advisory and transactional work to all forms of commercial litigation and arbitration.

Hill Dickinson’s life sciences team provides practical, commercial legal advice to companies at all stages of development, from start-up to established multinational.

Clients are supported from an idea in a lab, to helping incorporate the company, raising capital, protecting and licensing intellectual property, signing strategic partnerships and, ultimately, commercialising life-changing treatments and technologies.

The interdisciplinary team, based at offices in London, Manchester, Liverpool and Leeds, as well as internationally, blends insight and pragmatism to provide high-quality, trusted advice to some of the world’s leading life sciences companies.

For more information about the team, visit https://www.hilldickinson.com/sectors/life-sciences

For further information about the firm, visit hilldickinson.com

About Peterhouse Capital

Peterhouse provides integrated financial services – Corporate Finance, Corporate Broking, a Matched Bargain facility and Securities Trading – to companies which are listed on, or looking to join, the Standard List of the Main Market, AIM, the Aquis Exchange, or IPSX.

Peterhouse is the #1 London-based independent investment bank, as well as the leading independent small cap broker for AIM companies, and has completed, on average, one Client fundraise per week for three years running.

Peterhouse is also the largest AQSE Corporate Adviser, and its advisory business is known for problem-solving and pioneering new initiatives. These include:

- Supporting the first public company to undertake an ICO

- Listing the first UK medicinal cannabis investment company & the first cannabis IPO on the London Stock Exchange

- Structuring the first Aquis Exchange bond issue

- Introduced the first Canadian Stock Exchange/Aquis Exchange fast track dual listing

The Peterhouse team works closely with clients to provide them with pertinent and meaningful advice and bespoke solutions, whether on routine public company matters or in the context of complex corporate transactions.

For further information about the firm, visit https://peterhousecap.com

About Prohibition Partners

Prohibition Partners unlocks the potential of cannabis through data, intelligence and networking. We provide strategic solutions to an international client base of investors, operators, blue-chip companies, FMCG brands and government bodies.

Prohibition Partners’ experienced consultancy team can offer cannabis-related businesses intending on floating with the essential information and strategic services needed to prepare for a successful IPO on the London Stock Exchange.

Learn more about our consultancy services, here.

Prohibition Partners’ services include:

- Expert independent market analysis

- Consultancy

- Due diligence

- Risk analysis

- Competitor benchmarking

- Investor presentations

- Strategic planning

- Investor promotion

- Dedicated events and publications

- Networking and partnerships